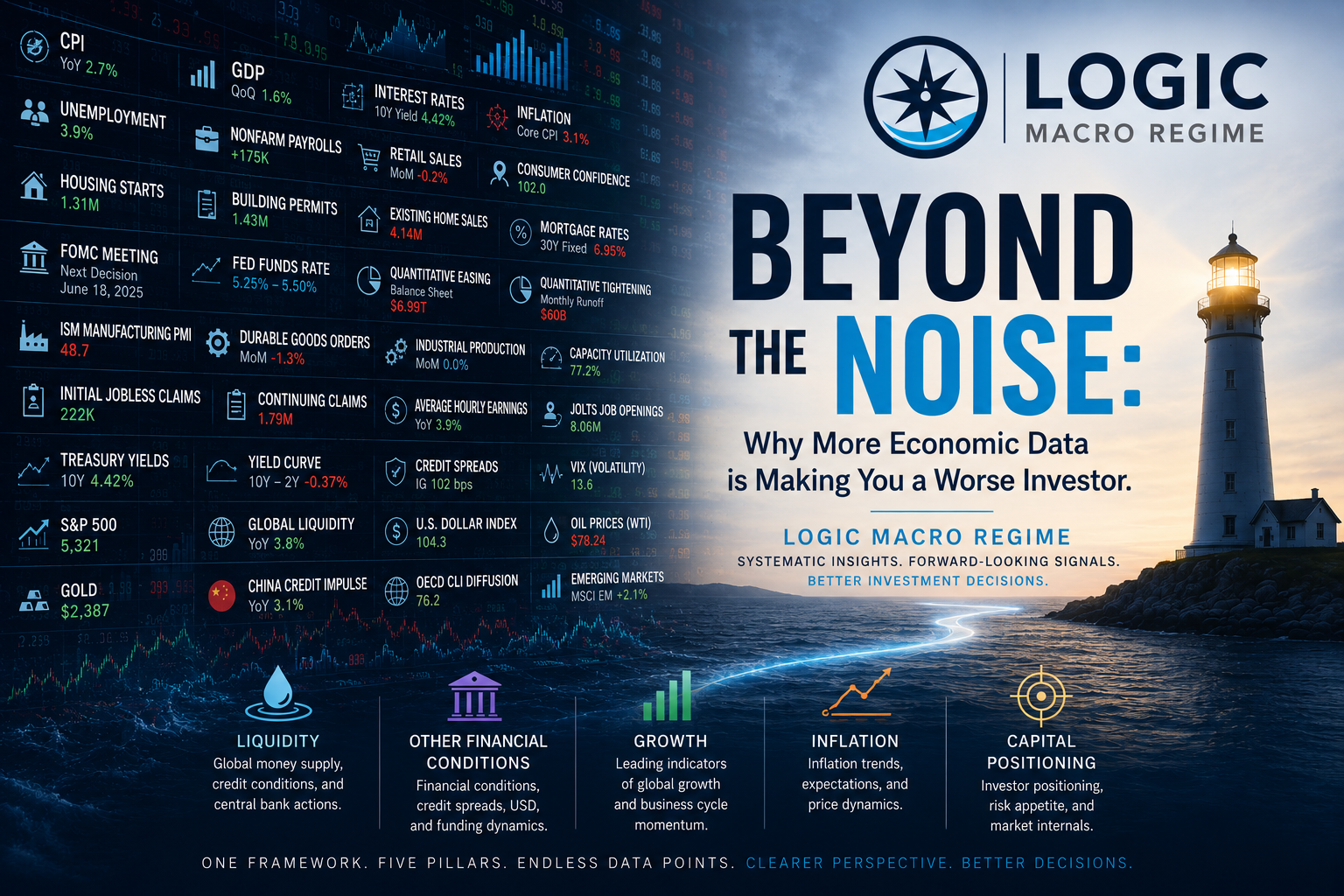

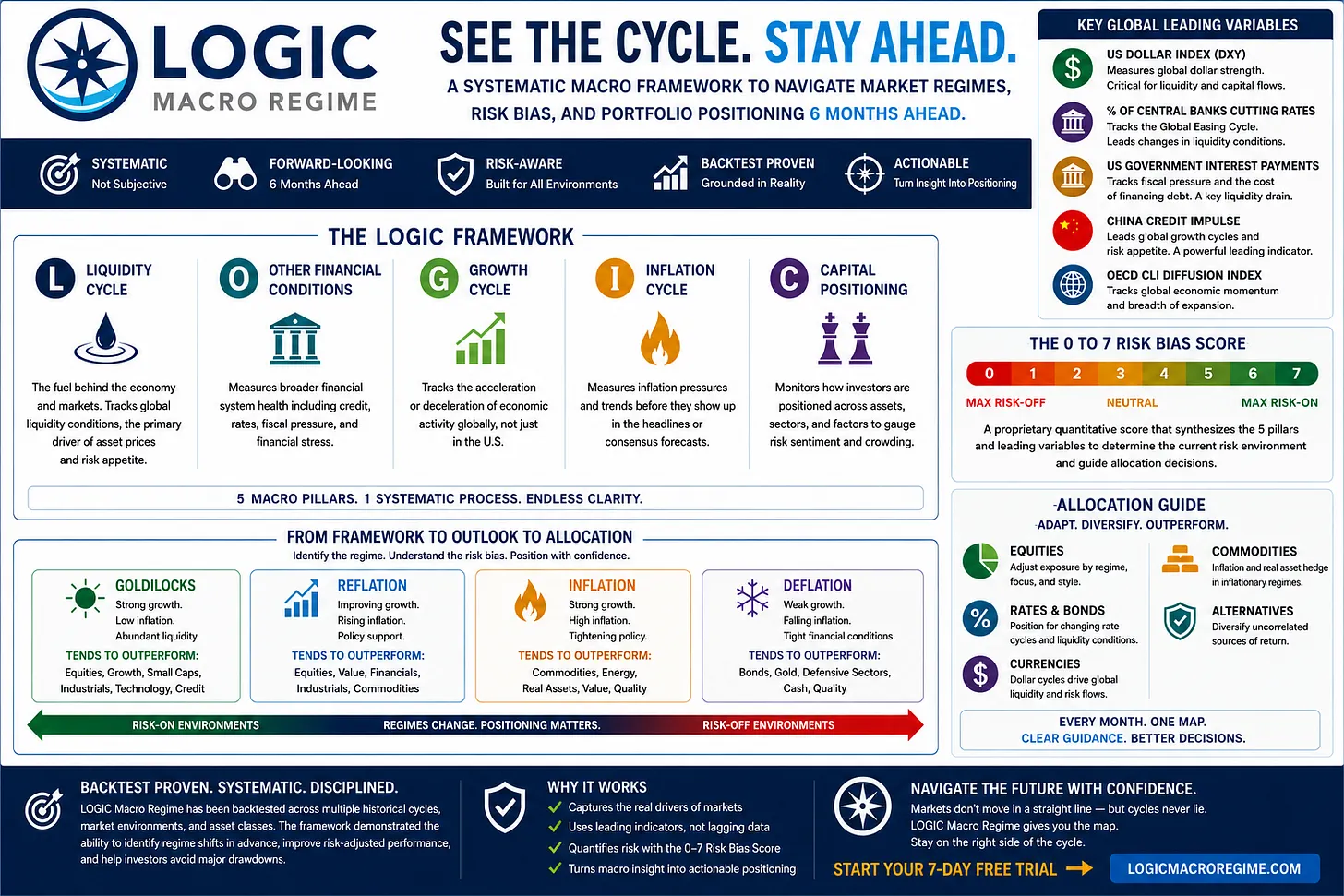

A synthesized view of how key macro variables interact to pinpoint where we are in the cycle.

Ahoy!

LOGIC Macro Regime converts sophisticated macro strategy into a systematic positioning tool. Trusted by institutional investors.

Stop guessing, navigate. Know where we are in the cycle, what regime is in play, and how to strategically position portfolio allocation and risk.

Presented through the interactive Monthly Macro Map dashboard.

Please note this is a lagged sample report that all LOGIC Macro Regime subscribers received well before the referenced month began.

April 2026 Snapshot

April, just like March, continues with a temporary air pocket for growth. What is notable is the shift in the inflation outlook, as our base case had been deflationary, but recent developments are beginning to challenge that view. The disruption in the Strait of Hormuz, through which roughly 20% of global oil supply flows, triggered a sharp spike in energy prices, with WTI crude oil briefly surging near $120 per barrel before settling back into the high $80s. While prices have retraced, the move itself is important as it signals that input cost pressures are re-emerging, particularly through energy, which has broad second-order effects across the economy. As a result, the near term inflation impulse is turning more positive, and April is now increasingly shaping up to be inflationary rather than deflationary. The longer this war drags on, the more risk that the Risk-On Goldilocks bias call from May to August 2026 ✅ may not come to pass. Interestingly enough, given all this geopolitical uncertainty, the S&P 500 is only down ~6% from its all-time high of 7,002 on January 28. Remember, Geopolitical > Macro in the short-term, but Macro wins out over multi-month timelines. As mentioned last month, more concerning macro Risk-Off clouds appear to be gathering for September and look to be continuing into October ❌. We will keep our community aware of this potential turn in future updates.

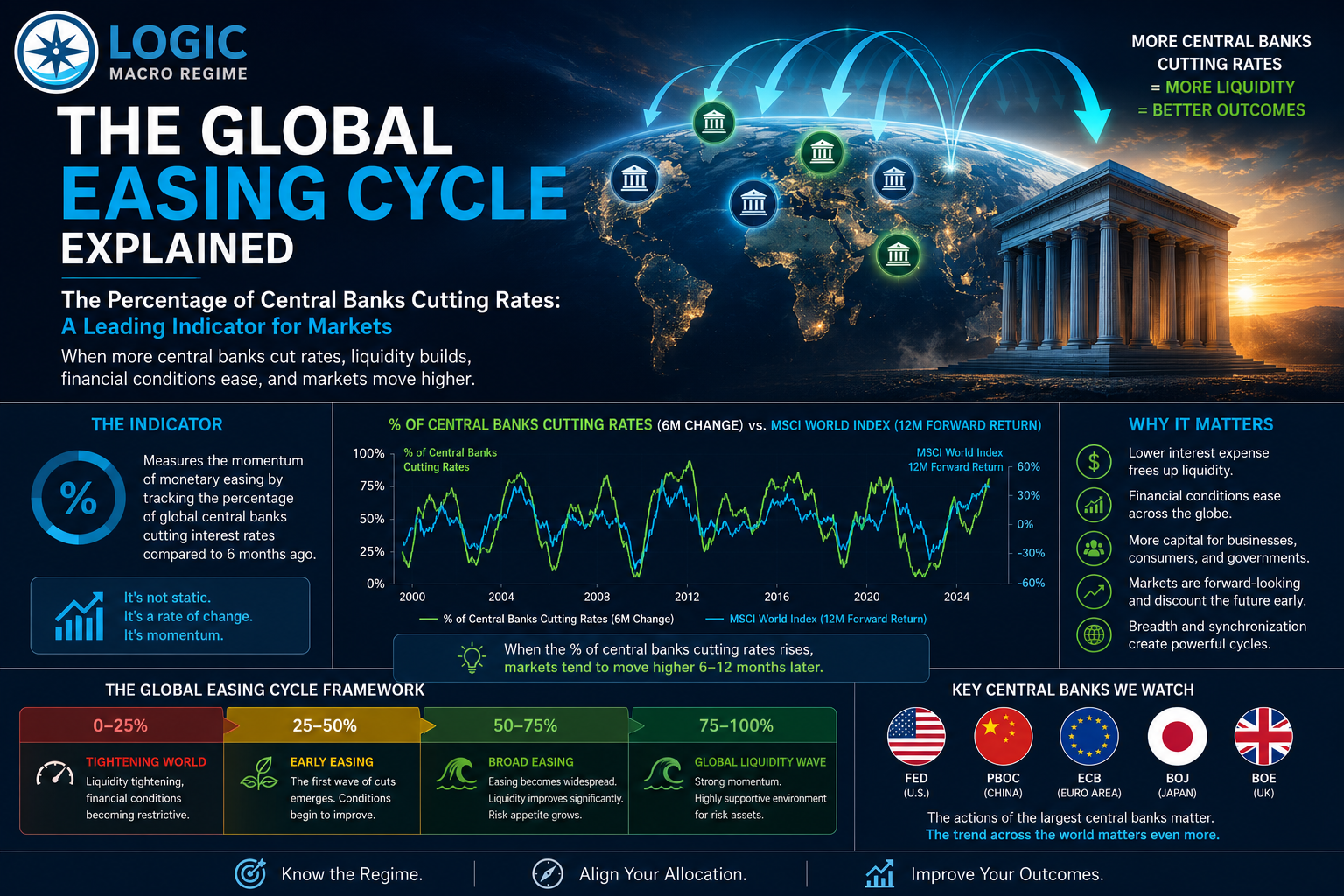

(L) Liquidity Cycle ✅

Global liquidity remains modestly supportive, though the rate of improvement is slowing. The US Federal Reserve balance sheet has stabilized and edged slightly higher to approximately $6.66 trillion. Ongoing ~$40 billion per month in Treasury bill purchases continue to support bank reserves and short-term funding conditions. However, this pace is expected to moderate following tax season, implying a deceleration in liquidity injection rather than further expansion. Importantly, the Fed's actions remain focused on reserve management and balance sheet composition, not broad-based stimulus. Liquidity is being maintained, but not meaningfully increased. Globally, China remains in a reflationary posture, though recent activity suggests less incremental acceleration, reinforcing a backdrop of steady, but not strengthening global liquidity.

(O) Other Financial Conditions ❌

Other financial conditions are beginning to tighten meaningfully, driven by a convergence of key inputs. The recent spike in oil, the master resource of the economy, is feeding directly into higher input and transportation costs, reinforcing that energy is a core driver of economic activity. At the same time, the US dollar is strengthening as a safe haven, tightening global liquidity conditions, particularly for non-US economies. Compounding this, interest rates are moving higher (+0.3% month-over-month to ~4.4% yield on the US 10-Year Treasury Bond), increasing the cost of capital and financing across the system. Together, these three forces are deteriorating financial conditions, making it more expensive to conduct business and service debt in an already highly leveraged, debt-based economy. As financial conditions tighten, they effectively drain purchasing power, reducing the amount of capital available for goods, services, and financial assets.

(G) Growth Cycle ⬆️

Growth remains durable over the longer term, supported by continued earnings expansion in the S&P 500, which reinforces the underlying strength of the cycle. However, the picture is becoming less uniform, with emerging air pockets beginning to appear. As noted, geopolitical tensions are creating disruptions in global trade and contributing to higher energy costs, introducing near-term volatility within an otherwise resilient growth backdrop. Although there could be some continued weakness coming in April, the longer trends show over 88% of the OECD's Composite Leading Indicators for global economies have positive month-over-month readings. These leading economic indicators (which is what we care most about) point to a global growth re-acceleration, especially if a cease fire or de-escalation occurs in Iran in the near term.

(I) Inflation Cycle ⬆️

The inflation backdrop is beginning to shift after a period of consistent cooling, with recent developments pointing to a re-emergence of near-term price pressures. While inflation had been trending lower across major economies, supportive for risk assets, that direction is now being challenged. The disruption in the Strait of Hormuz, through which roughly 20% of global oil supply flows, triggered a sharp spike in energy prices, with WTI briefly moving near $120 before settling back into the high $80s. Although prices have retraced, the move highlights how quickly input costs can reprice, particularly in energy, which feeds through broadly across transportation, production, and consumer prices. As a result, while the longer-term disinflation trend is not fully broken, the rate-of-change is turning more positive in the near term, suggesting inflation is no longer cleanly cooling. Similar to the above, if a cease-fire or de-escalation occurs in Iran, the more durable macro tides point to a continued easing of inflationary pressures heading into October.

(C) Capital Positioning ❌

Capital positioning has shifted from moderately bullish to defensively skewed following the geopolitical shock, with investors de-risking and reducing overall exposure. This reset lowers the risk of crowding and creates a more asymmetric setup, where any de-escalation or stabilization in tensions could trigger a sharp snap-back rally as sidelined capital is redeployed. However, this more risk-adverse positioning could be the start of a more lasting correction, which we don't believe is the case due to the strong underlying macro conditions (still in "Risk-On”), with growth holding up and inflation broadly easing outside of the recent energy-driven spike. We're not quite late-cycle yet, but more defensive posturing may be warranted. More concerning is what could be approaching in September and October as we are seeing some weakness beginning to form in these months for risk appetite - "Risk-Off” in the Monthly Macro Map.

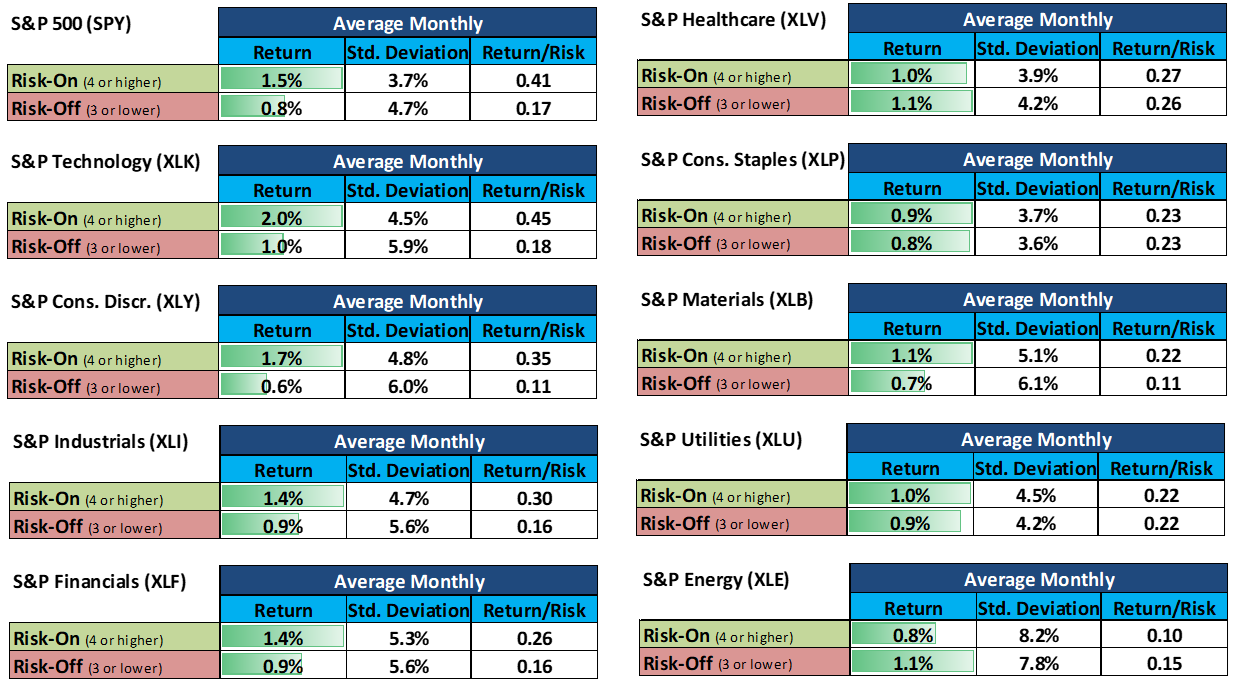

You can visit the website for asset, style, and sector factors that historically have out/under-performed in this kind of Macro Regime - Back-Test.

You can also see our past Blogs.