2011–2026

S&P sector behavior from September 2011 through March 2026.

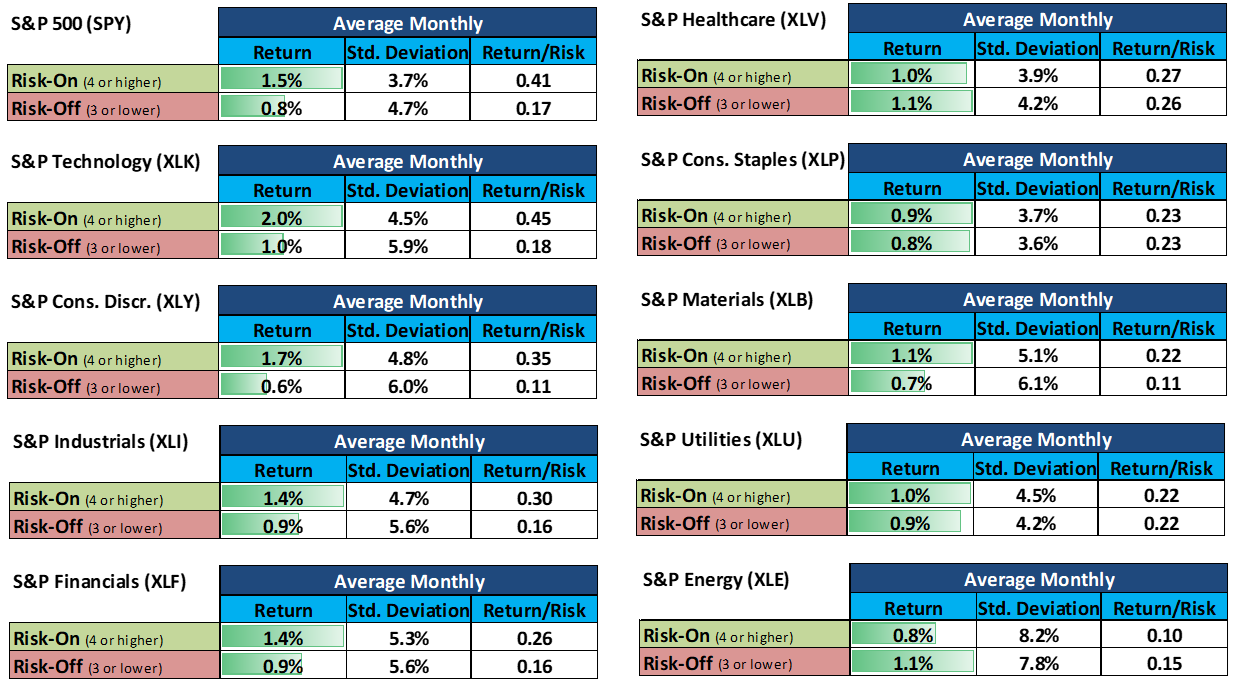

Most portfolios are built for markets that keep rewarding risk. This page shows what the historical data looks like when you separate the environment into Risk-On and Risk-Off instead of averaging everything together.

The point is not to call every market move. The point is to avoid owning a portfolio that is mismatched with the environment. In Risk-On periods, broad equity exposure and cyclicals are generally rewarded. In Risk-Off periods, returns usually slow, volatility rises, and portfolios often become far less efficient.

That is the key takeaway from the back-test. For the S&P 500, average monthly return drops from 1.5% in Risk-On to 0.8% in Risk-Off, while volatility rises from 3.7% to 4.7%. Return per unit of risk falls from 0.41 to 0.17. The damage is not always a crash. Often it is prolonged undercompensated risk.

The sectors that tend to hold up best in Risk-Off are the defensive core: Healthcare, Consumer Staples, and Utilities, with Energy as the notable exception when the stress is driven by supply-side shocks. By contrast, Technology, Consumer Discretionary, Industrials, and Materials tend to see a much larger deterioration in efficiency when the risk bias turns.

This table shows how major S&P sectors (ETF ticker tested) performed.

Below is a list of how major equity style factors, sectors and fixed income categories have tended to behave in each LOGIC Macro Regime. Historical tendencies only “ not a guarantee of future results and not investment advice.

Use this matrix as a practical guide to identify which asset classes, equity styles, sectors, and fixed income sectors have historically been favored in each Macro Regime and Risk Bias. The current Jun 2026 map highlights the active Risk-On / Reflation column.

| Category | Goldilocks | Reflation | Inflation | Deflation |

|---|---|---|---|---|

| Asset Classes | Stocks (VT), Bonds (BND)>Commodities (DBC), Cash | Stocks (VT), Commodities (DBC)>Bonds (BND), Cash | Commodities (DBC), Stocks (VT)>Bonds (BND), Cash | Bonds (BND), Cash>Stocks (VT), Commodities (DBC) |

| Equity Styles |

|

|

|

|

| Equity Sectors |

|

|

|

|

| Fixed Income Sectors |

|

|

|

|

| Category | Goldilocks | Reflation | Inflation | Deflation |

|---|---|---|---|---|

| Asset Classes | Stocks (VT), Bonds (BND)>Commodities (DBC), Cash | Stocks (VT), Commodities (DBC)>Bonds (BND), Cash | Commodities (DBC), Cash>Stocks (VT), Bonds (BND) | Bonds (BND), Cash>Stocks (VT), Commodities (DBC) |

| Equity Styles |

|

|

|

|

| Equity Sectors |

|

|

|

|

| Fixed Income Sectors |

|

|

|

|

Investors usually spend too much time trying to pick the right asset and not enough time asking whether that asset fits the regime. The bigger source of underperformance is often not being wrong on a stock. It is being wrong on the environment.

The Monthly Macro Map is designed to classify the environment ahead of time so you can stay invested with exposures that better match the Macro Regime and Risk Bias instead of reacting after the fact.