Most portfolios aren't built for “Risk-Off."

They're built for things continuing to work.

Growth holds. Inflation fades. Policy eases. Risk assets grind higher.

And when that changes, the damage isn't always obvious at first.

It shows up more quietly:

Returns slow

Volatility rises

And portfolios become less efficient

That last part matters the most.

Because once return per unit of risk collapses, compounding breaks.

What the data actually shows

We looked at S&P 500 sectors from September 2011 through March 2026.

But instead of averaging everything together, we split the world into two simple states:

"Risk-On” (Risk Bias Score “” 4)

“Risk-Off” (Risk Bias Score “” 3)

The difference is meaningful.

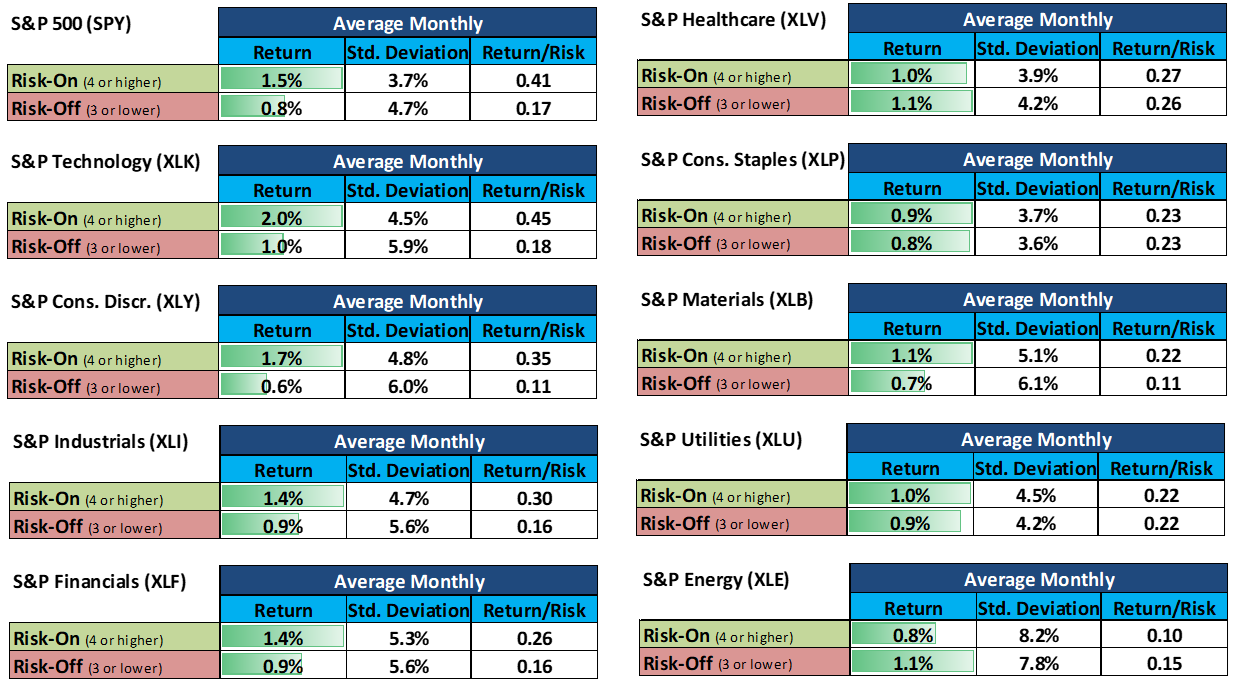

For the S&P 500:

- Risk-On: +1.5% per month, 3.7% volatility, 0.41 return/risk

- Risk-Off: +0.8% per month, 4.7% volatility, 0.17 return/risk

That's the shift.

You are taking more risk, for less than half the efficiency.

This is how portfolios struggle. Not necessarily through sharp drawdowns, but through prolonged periods of undercompensated risk.

The real issue: portfolios stay positioned for Risk-On

Most portfolios remain tilted toward:

Technology

Consumer Discretionary

Cyclicals more broadly

That makes sense in a "Risk-On” environment.

But in "Risk-Off,” the profile changes quickly.

Technology still produces returns, but with meaningfully higher volatility and much lower efficiency.

Consumer Discretionary sees one of the largest drops in return per unit of risk.

Industrials and Materials follow a similar pattern.

The issue isn't that these sectors stop working entirely.

It's that they stop paying you for the risk you're taking.

What actually holds up in "Risk-Off"

Only a handful of sectors maintain stability when conditions tighten.

These tend to form the defensive core of a portfolio:

- Healthcare (XLV)

Demand is relatively stable and less sensitive to the cycle. Performance holds up across regimes. - Consumer Staples (XLP)

Consistent earnings, lower volatility, and steady return profiles. - Utilities (XLU)

Lower beta and a stabilizing effect when financial conditions tighten. - Energy (XLE)

The exception. Performance often improves in "Risk-Off,” particularly when stress is driven by supply-side shocks - much like the environment of today.

These sectors are not designed to outperform aggressively.

They are there to preserve efficiency when the broader environment becomes more constrained.

This isn't about sector rotation

It's about avoiding a mismatch between your portfolio and the environment.

In "Risk-On,” aggressive positioning is rewarded.

In "Risk-Off,” that same positioning becomes a drag.

Defensive exposure isn't a late-cycle trade or a tactical add-on.

It's what keeps the portfolio functioning when conditions shift.

The challenge is timing

All of this is relatively easy to observe in hindsight.

The real difficulty is knowing when the risk bias is changing.

Because by the time "Risk-Off” is obvious in returns, the damage has already been done.

That's the problem this framework is designed to solve.

A forward-looking approach

At LOGIC Macro Regime, each month is scored ahead of time, through seven proprietary indicators that aggregate from 0-7.

Again, "Risk-On” (Risk Bias Score “” 4) and “Risk-Off” (Risk Bias Score “” 3).

The result is a forward classification of the environment:

"Risk-On” or "Risk-Off"

The goal isn't to predict markets precisely.

It's to understand the conditions you are stepping into, and align exposure accordingly.

What this means in practice

If the backdrop is "Risk-Off":

- reduce exposure to cyclicals

- trim aggressive positioning

- increase allocation to defensives

- focus on maintaining return per unit of risk

The objective isn't to avoid markets.

It's to stay invested, but in a way that fits the regime.

The bottom line

Most investors spend their time trying to pick the right assets.

But the more important question is whether those assets fit the regime and risk bias you are in.

Because the biggest source of underperformance is not being wrong on a stock.

It's being wrong on the environment.

If you want to see the regime and risk bias before the month begins, I publish the Monthly Macro Map. Come join the LOGIC Macro Regime community by subscribing:

LOGIC Macro Regime