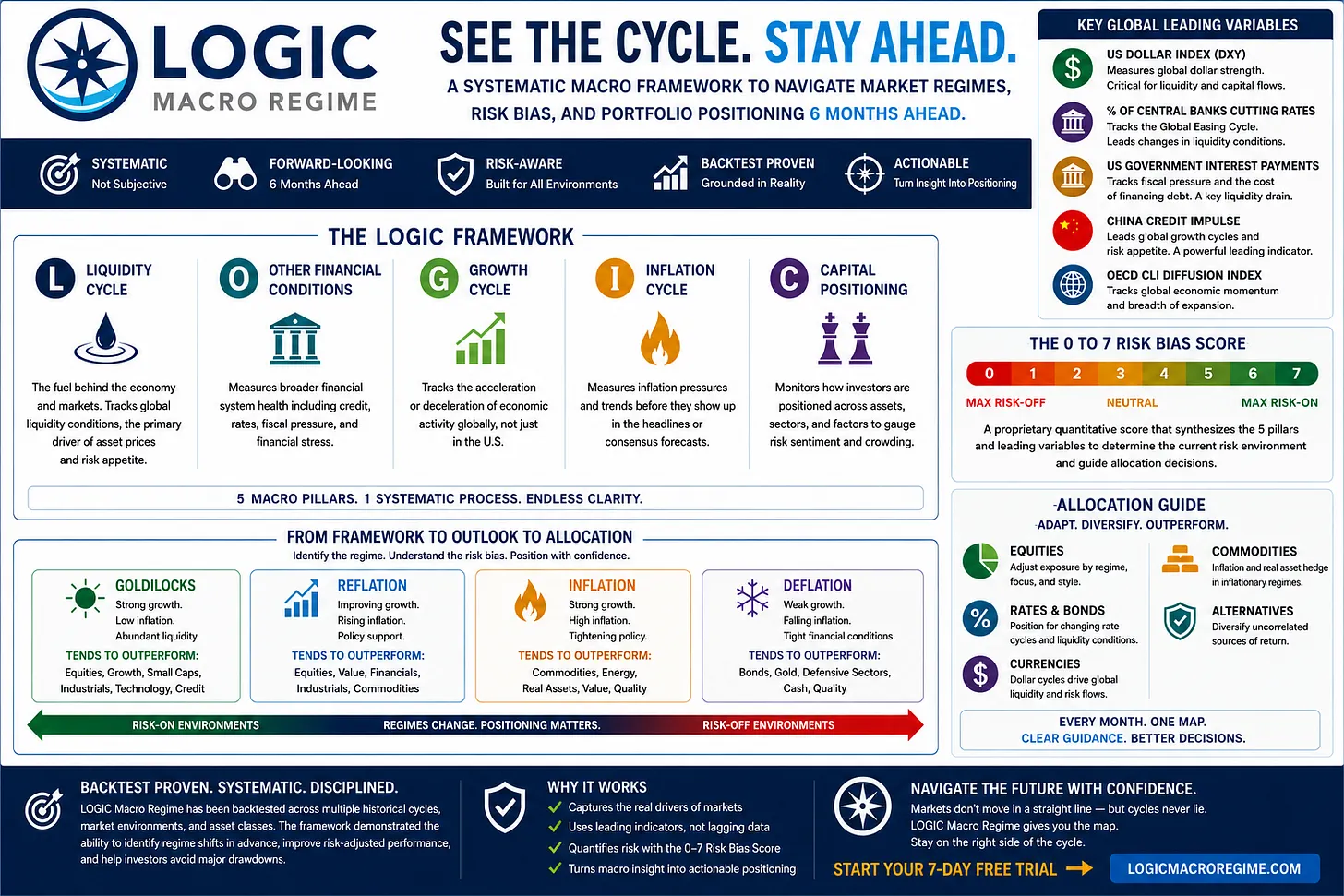

The Channel Matters: Understanding Other Financial Conditions

The institutional landscape is littered with the carcasses of portfolios that mistook a growing central bank balance sheet for a definitive green light for risk. We have all seen the screen: the headlines scream about a fresh injection of "global liquidity,” yet the indices remain paralyzed or, worse, roll over. This is the Liquidity Illusion. To the uninitiated, more money always equals higher prices. To the systematic macro strategist, liquidity is merely potential energy.

Within our LOGIC framework, liquidity is the fuel, but the "O” - Other Financial Conditions represents the channel through which that fuel must flow. As we established in our foundational pieces, "The Global Liquidity Cycle Explained" and "The Market's Biggest Misread: A Falling Dollar Is Bullish," liquidity is the primary driver of market cycles. However, even the highest-octane fuel is useless if the fuel lines are clogged or the valve is shut.

To master asset allocation, one must recognize that while liquidity powers the markets, financial conditions determine whether the engine can actually run.

The US Dollar is the Global Liquidity Valve

The US Dollar Index (DXY) is not merely a currency cross; it is the primary gatekeeper of the global financial system. Because the dollar serves as the world's reserve currency and the denomination for the vast majority of global debt and trade, its strength or weakness acts as a massive valve that either restricts or releases liquidity into the world.

When the dollar falls, it triggers a powerful easing mechanism. It reduces the debt-servicing burden for foreign entities holding trillion-dollar short positions (in the form of dollar-denominated debt) and lowers the cost of international trade. This is why a weakening dollar forces a shift in Capital Positioning (the "C” in LOGIC) away from defensive US Large Caps and into higher-beta emerging markets and global risk assets. Conversely, a surging dollar narrows the channel, forcing a "risk-off” retreat as the cost of liquidity becomes prohibitively expensive for the rest of the world.

The direction and momentum of the US Dollar Index matter far more than its absolute price level; it is the rate of change that dictates the speed of global liquidity transmission.

Tracking the DXY is about monitoring the opening and closing of this global valve. In a systematic macro investing context, we don't care about the academic "fair value” of the dollar; we care about whether the valve is opening wide enough to allow liquidity to flood into risk-on assets.

Credit Spreads and the "Loans Create Deposits” Reality

If the US Dollar is the valve, credit spreads - the difference between "safe” government yields and "risky” corporate yields - are the diagnostic tool for the health of the transmission mechanism itself. To understand why liquidity often feels "trapped,” we must move beyond the myth that central banks "print” money that goes directly into the economy.

The institutional reality is that "Loans create deposits.” Central bank liquidity exists primarily as bank reserves - potential energy sitting on a ledger. For that liquidity to enter the real economy and impact macro investing outcomes, the private banking system must be willing to extend credit. Tightening spreads indicate that the "risk-on” appetite of the banking sector is healthy, allowing liquidity to flow efficiently from lenders to borrowers. Widening spreads, however, signal that the channel is being blocked by fear.

The transmission mechanism breaks down when banks prioritize capital preservation over credit extension. Even if a central bank aggressively expands its balance sheet, liquidity remains trapped within the financial plumbing if commercial banks refuse to lend. In this scenario, the "fuel” stays stuck in the tank because the banks - the primary mechanics of the system - have shut down the pumps.

When spreads widen, the availability of liquidity becomes irrelevant because the transmission mechanism has failed. This is the "hidden mechanism” that retail investors often miss: you can flood a engine with fuel, but if the injectors are clogged, the car won't move. This is why credit spread momentum is a non-negotiable component of our macro regime tracking.

Energy Prices are the Global Economy's Master Tax

If we view financial conditions as a physical channel, energy prices - specifically oil - represent the debris that determines the level of friction within that channel. Oil is the "master resource"; its price is embedded in the cost of every physical good and service on the planet.

High energy prices function as a mandatory, regressive tax on every consumer and business globally. When oil prices spike, they act like silt and debris physically clogging the pipe. No matter how much pressure (liquidity) the central banks apply, the sheer volume of "friction” created by high energy costs slows the flow of capital to a crawl. Discretionary income is diverted to staples, corporate margins are squeezed, and the channel narrows until growth begins to stall.

Conversely, falling energy prices act as a massive tailwind, clearing the debris from the channel. Lower costs for businesses and increased disposable income for consumers allow liquidity to translate into growth much more efficiently. By tracking energy price momentum, we can determine whether the global economy is facing a headwind or a push from behind, allowing us to adjust our asset allocation before the shift becomes obvious to the broader market.

Interest Rates are the Friction of Credit Creation

Interest rates are frequently mischaracterized as the "price of money.” In a systematic macro investing framework, we view them more accurately as the friction of credit creation.

There is a vital distinction between the availability of money (liquidity) and the cost of money (interest rates). Imagine a corporation with a $1 billion credit line. Liquidity is "available” to them. However, if the interest rate on that line is 9% while the company's internal rate of return (IRR) on a new project is only 7%, the cost of that money creates too much friction. The liquidity sits idle. High interest rates create a "crowding out” effect where debt servicing consumes the cash flow that would otherwise drive productive investment and market positioning.

When rates begin to ease, this friction decreases. Lowering the debt-servicing burden improves the efficiency of liquidity transmission, making it profitable for companies to borrow and invest again. This shift lowers the barrier to entry for capital deployment, signaling a change in the macro regime from contraction to expansion. We monitor rates to see when the path for capital is finally clear enough for aggressive deployment.

Momentum is the Ultimate Leading Indicator

The "Professional's Edge” in macro does not come from watching the news; it comes from quantifying the rate of change. The LOGIC framework prioritizes direction and momentum over absolute levels. It doesn't matter if oil is at $80 or $100 in a vacuum; what matters is whether it is moving toward $70 or $110.

Financial conditions are cyclical, and they lead the real economy. By tracking the momentum of these four pillars - DXY, Spreads, Energy, and Rates - we move from reactive, emotional headline-watching to a systematic approach to the liquidity cycle. This allows us to identify the transition between regimes with surgical precision.

Liquidity leads Growth.

Other Financial Conditions influence Capital Positioning.

By monitoring the "O,” we quantify how aggressively capital is being deployed and how efficiently liquidity is reaching the engine of the economy. This is the bridge to execution. When conditions are easing (DXY falling, spreads tightening, energy cooling, rates peaking), the channel is opening. This forces a shift in Capital Positioning toward risk-on assets. When conditions tighten, the channel closes, and the prudent strategist retreats to safety, regardless of what the central bank's "fuel” gauges say.

Conclusion: Mastering the Flow

Understanding the raw volume of global liquidity is only half the battle. To gain a true edge, you must understand the state of the channel. The "Other Financial Conditions” we have analyzed provide the necessary context to turn liquidity data into actionable asset allocation decisions.

The transmission of liquidity will always expand and contract in cycles. The strength of the LOGIC framework lies in its ability to systematically track these shifts, identifying when the channel is opening for a sustained rally or closing ahead of a sharp correction. As you survey today's market, look past the central bank headlines and ask: Is the channel widening, or is the friction of the "O” becoming too great for the fuel to flow?

Liquidity may power markets - but Other Financial Conditions determine whether the engine can actually run.