Ahoy!

LOGIC Macro Regime converts sophisticated macro strategy into a systematic positioning tool. Trusted by institutional investors.

Stop guessing, navigate. Know where we are in the cycle, what regime is in play, and how to strategically position portfolio allocation and risk.

Presented through the interactive Monthly Macro Map dashboard.

Please note this is a lagged sample report that all LOGIC Macro Regime subscribers received well before the referenced month began.

March 2026 Snapshot

- Macro Regime: Deflation

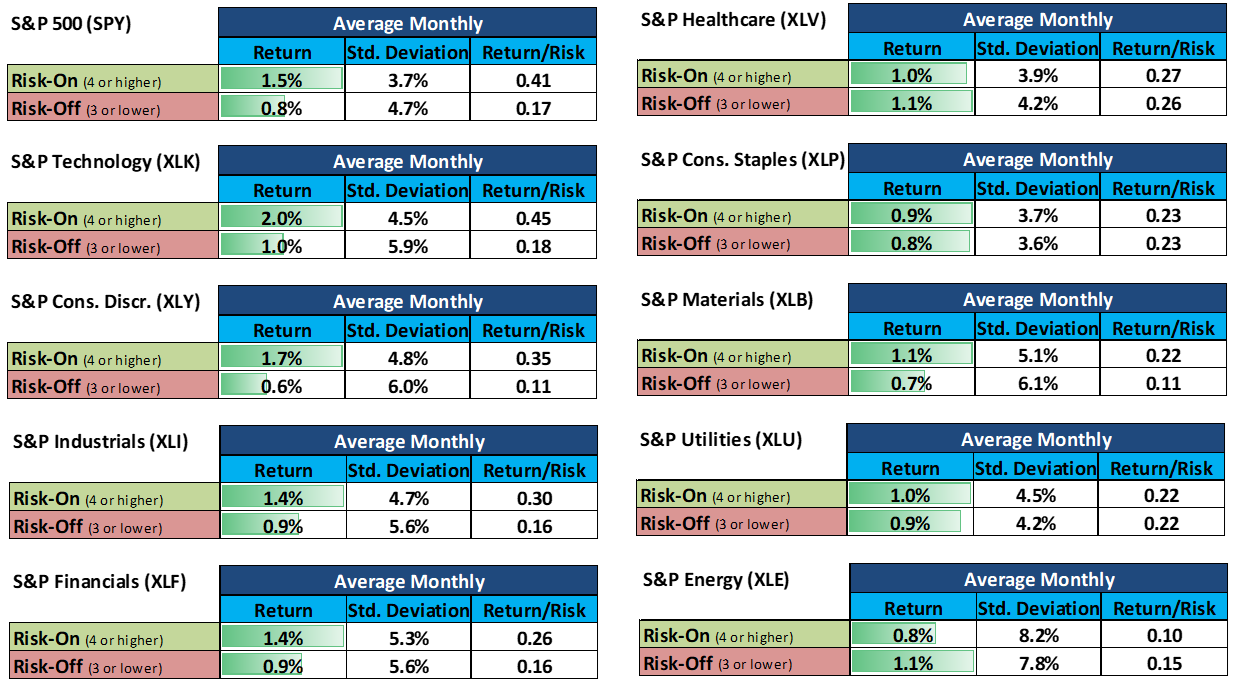

- Risk Bias Score: (5) Risk-On

- Forward View (6 months): March may bring a temporary air pocket for growth (Deflation), but its expected to be short with a Risk-On Goldilocks bias remaining intact afterwards from April to August 2026 ✅, then Risk-Off clouds appear to be gathering for September 2026❌. We will monitor the situation in coming months.

Importantly, this signal is not based on noisy short-term market moves or narratives'and these days there is no shortage of geopolitical headlines that continue to add volatility and whipsaw markets. Its moments like this when the LOGIC Crew steps back and objectively looks at the underlying tides that mechanically move markets. The conditions for the months ahead reflect the aggregate state of the Liquidity, Other Financial Conditions, Growth, Inflation, and Capital Positioning cycles, alongside key global leading variables. As of today, several market developments continue to reinforce, not contradict the current LOGIC signal, which is an improvement over last month's (7) Risk-On Goldilocks. Also, the 6-month outlook remains nearly identical to the Risk Bias and Macro Regime that was expected last month, although we can now roll forward to see that September may be setting up for risk.

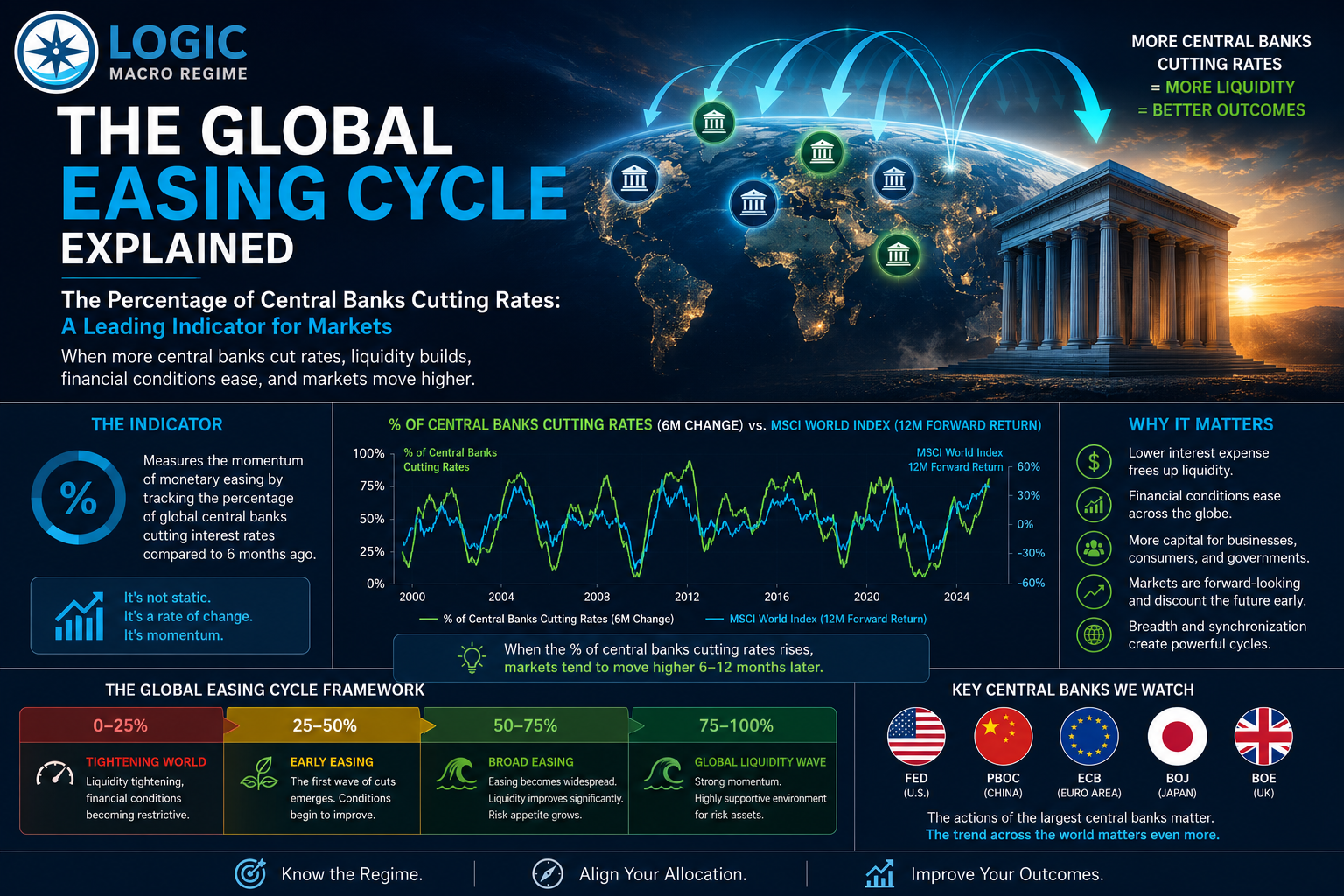

(L) Liquidity Cycle ✅

Global credit, base and broad-money supply continue to grow at a modest pace. We mentioned in December that the US Federal Reserve announced and has begun purchasing $40 billion per month of US Treasury Bills to manage bank reserve levels, which adds incremental liquidity. Overall, the tide of money remains supportive, likely to lift risk assets. The US Fed's total balance sheet assets were about $6.61 trillion as of mid-February, growth from the previous month to prove this is the case. The People's Bank of China (PBOC) balance sheet also expanded by $150 billion USD in the last month, showing their commitment to reflate the Chinese economy. Overall, the tide of money remains moderately supportive, likely to lift risk assets.

(O) Other Financial Conditions ❌

An elevated share of central banks are cutting policy rates, and expectations for further easing into 2026 have firmed. However, rate volatility is persisting in the Japanese Government Bond (JGB) market. We flagged this last month. The JGB market is important due to the carry trade. Further, the US dollar and oil prices have also climbed, making vital financial inputs more expensive. We will monitor this in coming months, but the weakening of Other Financial Conditions is broadly why the Risk Bias Score has dropped to 5 this month, from 7 the month before.

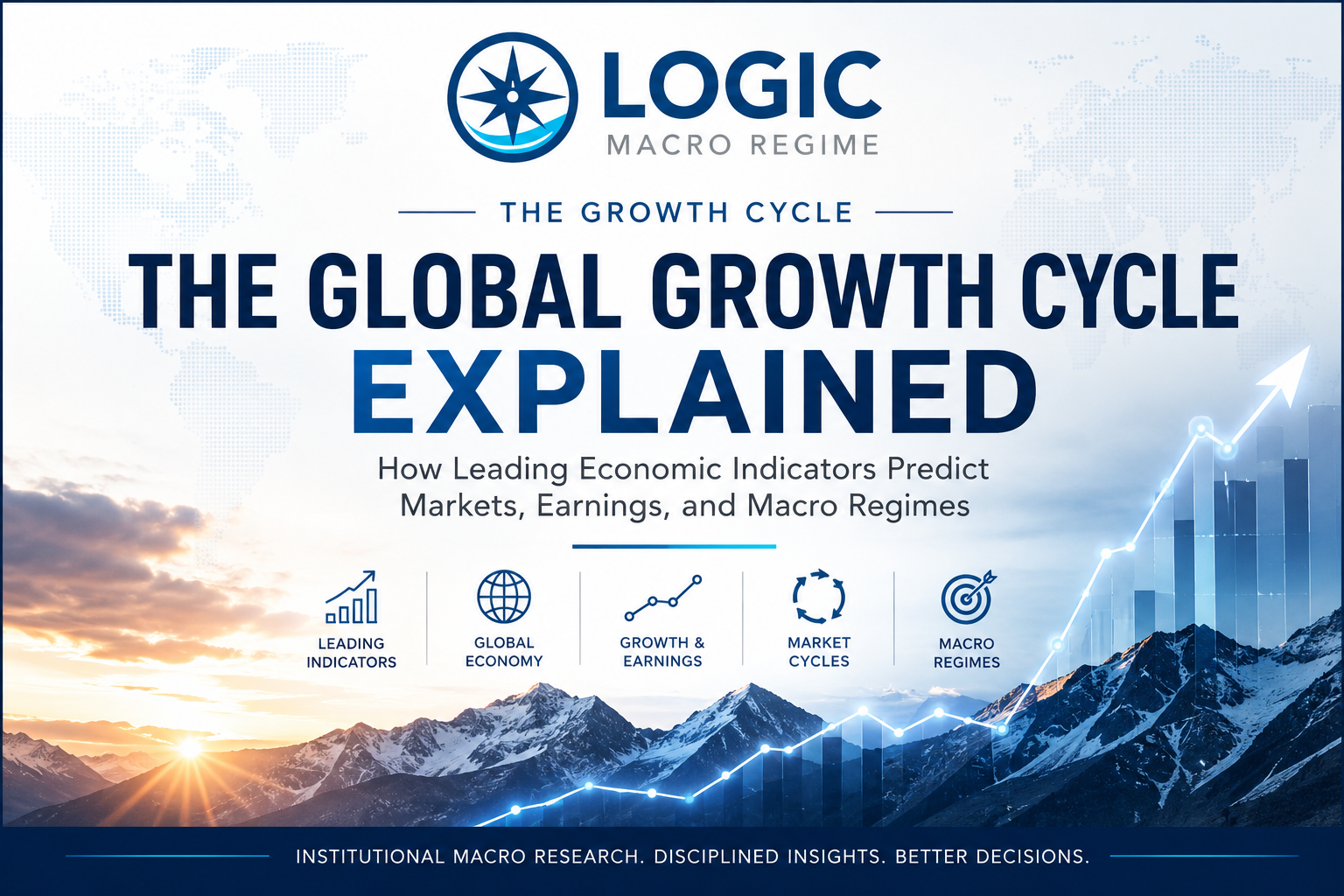

(G) Growth Cycle ⬆️

The growth picture is less clean than last month - but still strong on the aggregate. Although there could be some weakness coming in March, the longer trends show over 94% of the OECD's Composite Leading Indicators for global economies have positive month-over-month readings. These leading economic indicators (which is what we care most about) point to a global growth re-acceleration. This combination of resilient, improving growth (expected after March) alongside decelerating inflation is precisely what defines a Goldilocks environment in the LOGIC framework.

(I) Inflation Cycle ⬇️

Inflation continues to cool directionally across major economies - supportive for risk assets historically, because it gives central banks room to stay patient or ease further if needed. In the US, the US Bureau of Labor Statistics CPI for all items rose 2.4% year-over-year in January (down from 2.7% in December and considered a downside miss). In Canada, Statistics Canada reported CPI up 2.3% year-over-year in January 2026, with year-over-year price growth slowing in nine provinces compared to December. In Japan, Reuters reported January core inflation cooled to +2.0% (around the BOJ's target) - easing price pressure. The inflation tide is still flowing in a "cooling” direction. That doesn't mean inflation is gone - but the rate-of-change remains favorable as far out to September.

(C) Capital Positioning ✅

Despite strong asset gains in 2024-2025, investor positioning continues to remain far from all-in on our metrics. Capital remains selectively allocated rather than fully committed. Measures of leverage and speculative positioning are modest, and we aren't seeing the kind of rampant crowding or over-extension that typically precedes major market tops. What this means in plain language: the regime can remain Risk-On and still be prone to corrections. When positioning gets more crowded, markets can drop faster on surprises. We're not quite late-cycle yet, but could be approaching there in September if we see a string of Risk-Off months follow in subsequent Monthly Macro Maps. Once we see this turn in our leading indicators, we will telegraph it to our subscribers in advance.