Ahoy!

Please note this is a lagged sample report that all LOGIC Macro Regime subscribers received well before the referenced month began.

The conditions for the months ahead reflect the aggregate state of the Liquidity, Other Financial Conditions, Growth, Inflation, and Capital Positioning cycles, alongside key global leading variables. As of today, these signals point to the current LOGIC signal, which is a notable shift over last month's (5) Risk-On Inflation.

May 2026 Snapshot

April was marked by a surge in geopolitical volatility tied to the conflict in Iran and disruption through the Strait of Hormuz, which pushed oil prices higher, lifted inflation expectations, and drove a sell-off in bonds as yields rose and financial conditions tightened. This aligned with the short-term "air pocket” in growth we had flagged in March and April update emails, but importantly, we maintained throughout that the broader environment remained Risk-On, meaning any weakness was likely to be shallow and temporary rather than structural. That is exactly what played out, with the S&P 500 dropping to a low of 6,317 on March 30 (declining ~10% from its late-January highs), but holding in well and rebounding quickly to new all-time highs. This reinforced the resilience of risk assets even amid elevated uncertainty. Looking ahead, the regime path remains constructive, with Reflation in the near term transitioning into Goldilocks through August, both of which are supportive Risk-On environments. While September and October still represent the most likely window for a potential correction as Risk-Off conditions could briefly emerge, the broader outlook beyond that points back to Risk-On Goldilocks into November, suggesting any fall weakness would likely be a pause within an otherwise favorable macro backdrop.

(L) Liquidity Cycle ✅

Global liquidity remains moderately supportive, continuing to edge higher, though at a slower pace than earlier in the cycle. Central banks remain in a maintenance phase, ensuring that reserves and funding conditions remain stable without aggressively expanding balance sheets. This is an important distinction. Liquidity is not accelerating sharply, but it does not need to. The level remains sufficiently accommodative to support asset prices, reinforcing a stable foundation for risk-taking behavior and earnings growth. In this environment, liquidity acts as a steady tailwind, not a catalyst, but importantly not a constraint.

(O) Other Financial Conditions ❌

Other financial conditions tightened meaningfully over the past couple of months, acting as the primary driver behind the recent market volatility. The combination of rising oil prices, geopolitical disruption tied to the Strait of Hormuz and conflict in Iran, alongside higher bond yields, created a temporary tightening impulse. Higher rates reflected markets pricing in renewed inflation pressure, while energy shocks fed directly into input costs and inflation expectations. However, this tightening now appears to be easing at the margin. Oil prices have retraced from their peaks, bond yields have stabilized, and the US dollar has softened modestly. These developments suggest that the worst of the financial conditions tightening impulse is likely behind us, reducing the drag on growth and risk assets going forward.

(G) Growth Cycle ⬆️

Growth is re-accelerating. As flagged in the previous updates, the softness observed through March and April was expected to be a temporary air pocket, not the start of a broader downturn. That view is now being validated. Leading indicators and underlying economic momentum point to global growth regaining traction, reinforcing the reflation narrative in the near-term and supporting a transition toward a more balanced Goldilocks environment over the medium-term. This re-acceleration is critical. It confirms that the cycle remains intact and that recent volatility did not translate into longer-lasting economic weakness.

(I) Inflation Cycle ⬇️

Inflation has moved higher in the near term, largely driven by energy-related shocks, particularly oil. This increase reflects a transitory impulse, rather than a sustained structural shift. Energy remains a key driver of short-term inflation expectations, and the recent spike filtered quickly through transportation and input costs. However, with oil prices already retracing and broader disinflationary trends still in place from falling shelter costs and AI, the expectation remains that inflation will moderate over the coming months. Ceasefires appear to be desired to ensure interest rates don't levitate higher. This dynamic supports the current Reflation regime in the near term, while still allowing for a transition back toward Goldilocks conditions into June as inflation stabilizes.

(C) Capital Positioning ✅

Capital positioning experienced a rapid de-risking phase during the recent volatility, as investors responded to tightening financial conditions and geopolitical uncertainty. However, this reset has been constructive. Positioning is now far cleaner, and recent market behavior suggests capital is beginning to rotate back into risk assets. The speed of the equity market recovery reinforces this point. The S&P 500 correction was shallow and the subsequent rebound was both swift and decisive. This aligns directly with the prior call that any drawdown would likely be short-lived and met with strong buying interest. Positioning is now shifting back toward a more supportive stance, creating a healthier setup for forward returns. As we also consistently flagged last month, there are more concerning headwinds approaching in September and October as we are seeing a window of weakness open up - "Risk-Off” in the Monthly Macro Map.

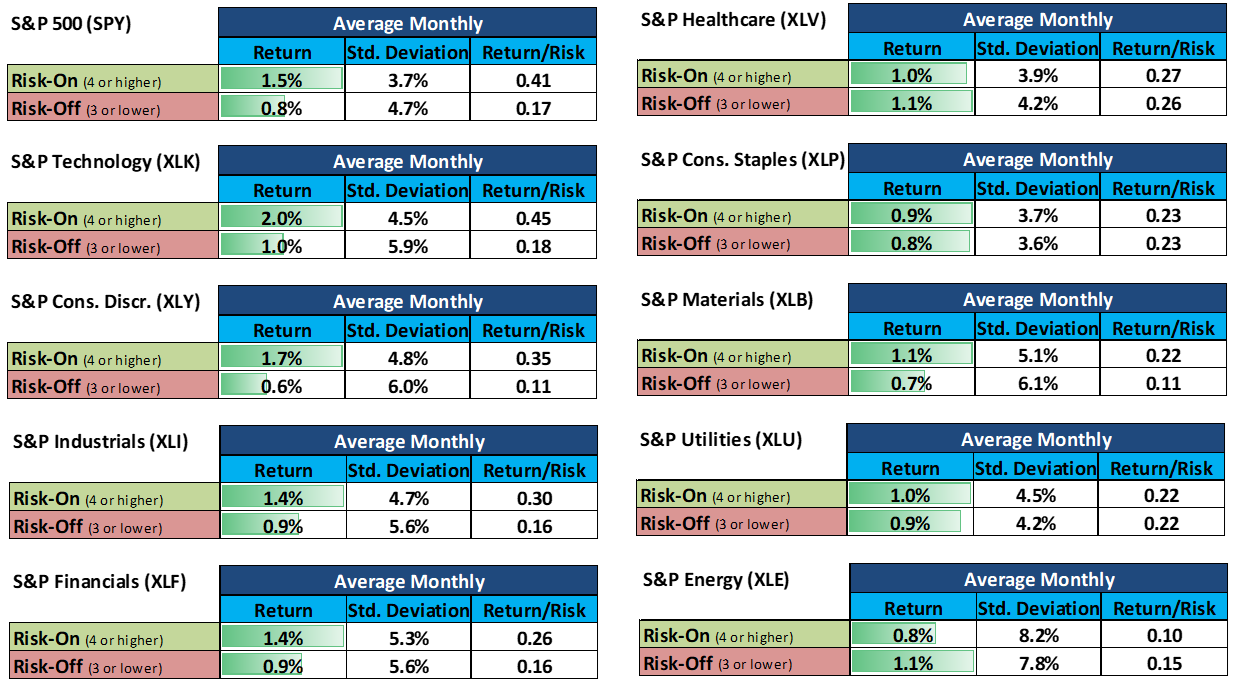

With Risk-On Reflation and Goldilocks on the horizon until August, allocating to overlapping styles/sectors like High Beta, Mega Cap Growth, Cyclicals, Small Caps, Consumer Discretionary, Technology, Financials and Industrials, could be a favorable strategy. BUT, remember, don't overstay your welcome as August may be the time to start trimming back on risk, in anticipation of the September/October window of weakness.

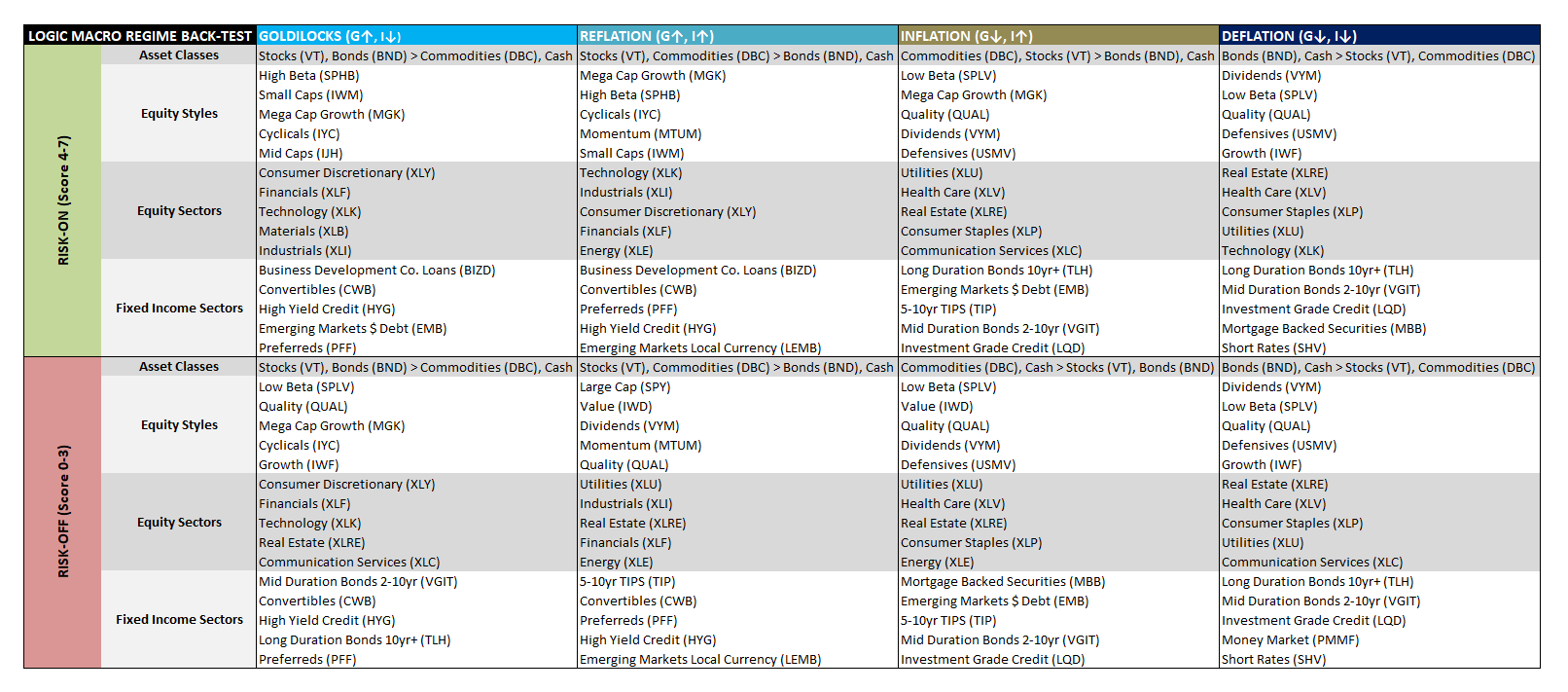

For even more insight on how to position (and to see the table in a larger format), you can click on Back-Test for asset, style, and sector factors that historically have out/under-performed in this kind of Macro Regime.