The "debt clock” has long been the favorite prop of financial alarmists. For decades, we have been told that the staggering rise in US national debt and the surging costs to service it are the precursors to an inevitable systemic collapse. Yet, a persistent and frustrating paradox remains for the bears: as the fiscal situation appears to deteriorate, equity markets frequently find the fuel to climb higher.

To the uninitiated, this decoupling looks like irrational exuberance or a broken market. To the institutional macro strategist, it reveals a deeper, mechanical reality. The US government is no longer merely a participant in the economy; it is the central actor in a global liquidity play. Within the LOGIC Macro Regime framework, we recognize that government interest payments - usually viewed as a catastrophic burden - are actually a premier leading indicator for the next market regime.

Understanding this engine is the difference between fighting the tide and riding the wave of global liquidity.

The US Government is the World's Largest "Short-Seller” of Dollars

In macro investing, debt is not just a liability; it is a massive, directional short position. Because the US government carries the largest debt burden in history, denominated entirely in its own currency, it has effectively become the world's largest entity "short” the US dollar.

Current debt-to-GDP levels have moved beyond historically sustainable norms, becoming structurally elevated. For a household, this would be a prelude to bankruptcy. For a sovereign issuer of a fiat currency, however, the endgame is entirely different. To manage a debt load that cannot be serviced in "real” terms, the issuer is mathematically incentivized to ensure the currency's value relative to that debt diminishes over time.

In a fiat system, a sovereign with unpayable nominal debts is structurally committed to the eventual dilution of its own currency.

The Accounting Identity: Your Deficit is My Surplus

The most common error in contemporary macro analysis is viewing the sovereign through a household lens. This is a category error of the highest order. A household is a currency user; the US government is the currency issuer. In a closed macro-accounting system, every penny the government "loses” is a penny the private sector "gains."

"The public sector deficit is the private sector surplus."

When the government runs a deficit - even one driven by the "wasteful” cost of interest payments - that capital does not vanish. It is deposited into the global financial system. Investors often miss this because they focus on the perceived "morality” of debt rather than the mechanics of the accounting identity. A surging deficit is essentially a massive, forced injection of capital into the non-government sector.

Why Rising Interest Costs Force the Hand of Policymakers

We have transitioned into a new era where an increasing share of fiscal spending is consumed by debt servicing rather than the "real” economy. This shift creates the Sovereign Liquidity Engine - a mechanical progression that leaves policymakers with no choice but to expand the money supply. We view this as a three-phase logical progression:

1. Phase 1: The Nominal Breaking Point

Interest costs rise until they begin to crowd out all other fiscal priorities, threatening the stability of the Treasury market and the broader transmission of policy.

2. Phase 2: The Policy Inflection

As the debt service burden threatens a "debt spiral," the pressure shifts from the Federal Reserve to the Treasury. Fiscal dominance takes hold.

3. Phase 3: The Liquidity Release

To prevent a systemic freeze, the system is forced toward debt monetization, monetary accommodation, and financial repression.

To alleviate the real burden of the debt, the sovereign (Federal Government aligned with the Fed) must ensure that liquidity is sufficient to keep the system functioning, effectively diluting the debt through the creation of new base money.

The Sovereign as the New Dominant Macro Actor

The post-GFC era marked a permanent shift in the global hierarchy. As the private sector underwent a decade of deleveraging, the burden of maintaining economic momentum moved to the sovereign balance sheet.

We are now in a regime of Fiscal Dominance. In this environment, the traditional business cycle and corporate earnings are secondary to government fiscal dynamics. The US Treasury has effectively become more influential than the Fed's Open Market Committee.

The US Treasury reinforced this dynamic beginning in late 2022 by aggressively issuing Treasury Bills - essentially cash-like instruments with minimal duration risk - to fund itself. This shift effectively injected liquidity back into the financial system and closely coincided with the bottom in US liquidity conditions and, shortly thereafter, the S&P 500.

Because the US dollar remains the global reserve currency, these US fiscal dynamics dictate global financial conditions. The sovereign is no longer just a regulator; it is the dominant macro actor whose balance sheet dictates the path of global markets.

Interest Payments as a "Secret Weapon” Leading Indicator

Most investors are distracted by noisy, coincident data like current GDP or last month's inflation prints. This is why they are perpetually blindsided by market pivots. Rising US government interest expense is a "secret weapon" because it is a mathematical necessity, not a survey-based projection.

Within LOGIC Macro Regime's framework, we track a specific causal chain:

Rising Government Interest Expense → Rising Liquidity to Service the Debt → Favorable Market Regimes & Risk-Biases

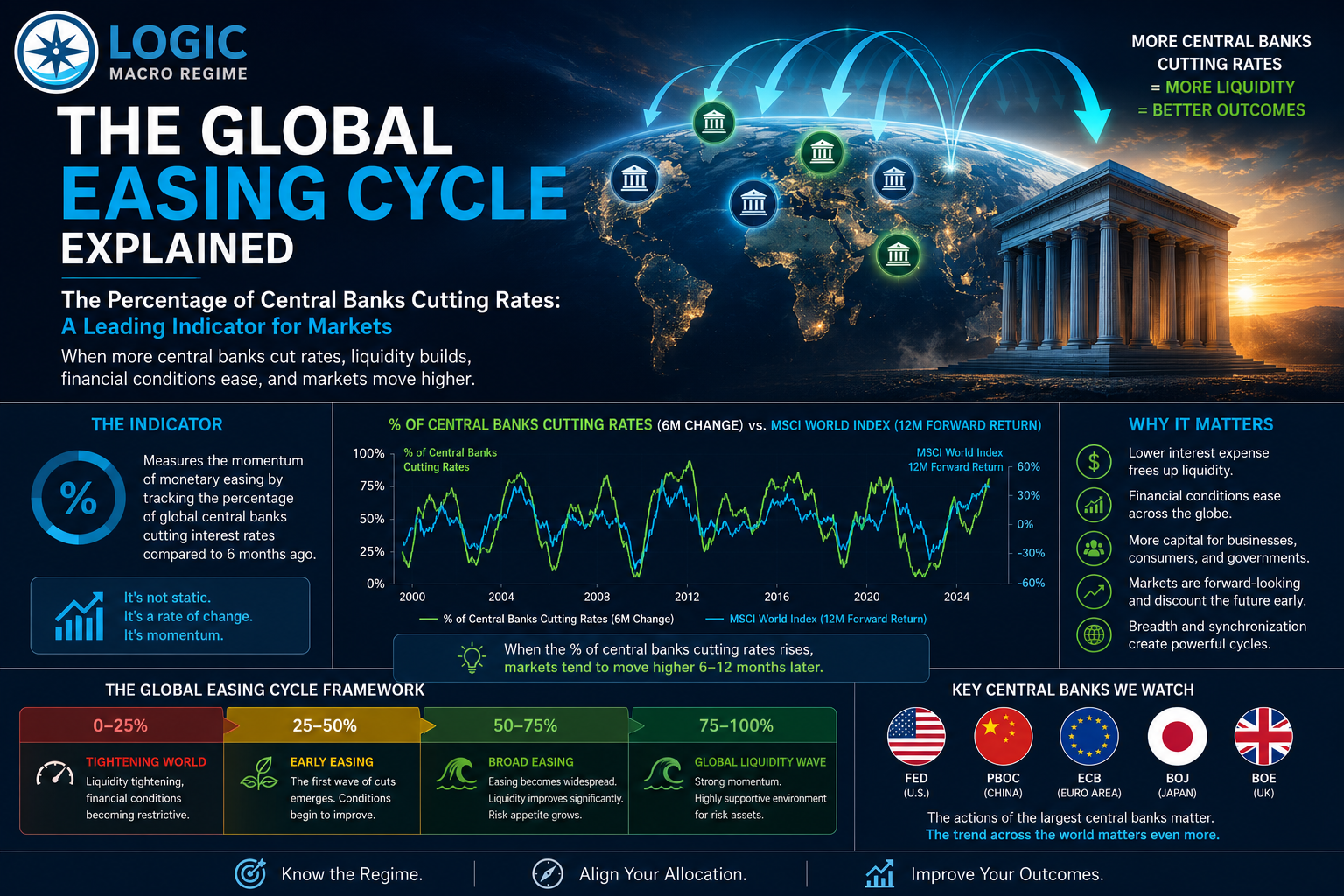

Rising interest costs are the first domino. They signal the mounting pressure that will necessitate the next injection of macro liquidity via the US Treasury and Fed. Historically, there is a meaningful lead time between the surge in interest costs and the subsequent surge in liquidity creation. Liquidity is the fuel that drives both the real economy and the financial economy. By tracking the interest burden today, we gain a forward-looking view of the liquidity conditions of tomorrow.

The Liquidity Flow into Financial Assets

In a highly financialized global economy, new liquidity does not distribute itself evenly. It follows the path of least resistance: financial assets. Because debt functions as collateral, the necessity of maintaining the value of that collateral means the "liquidity engine” often bypasses the real economy to hit brokerage accounts and institutional balance sheets first.

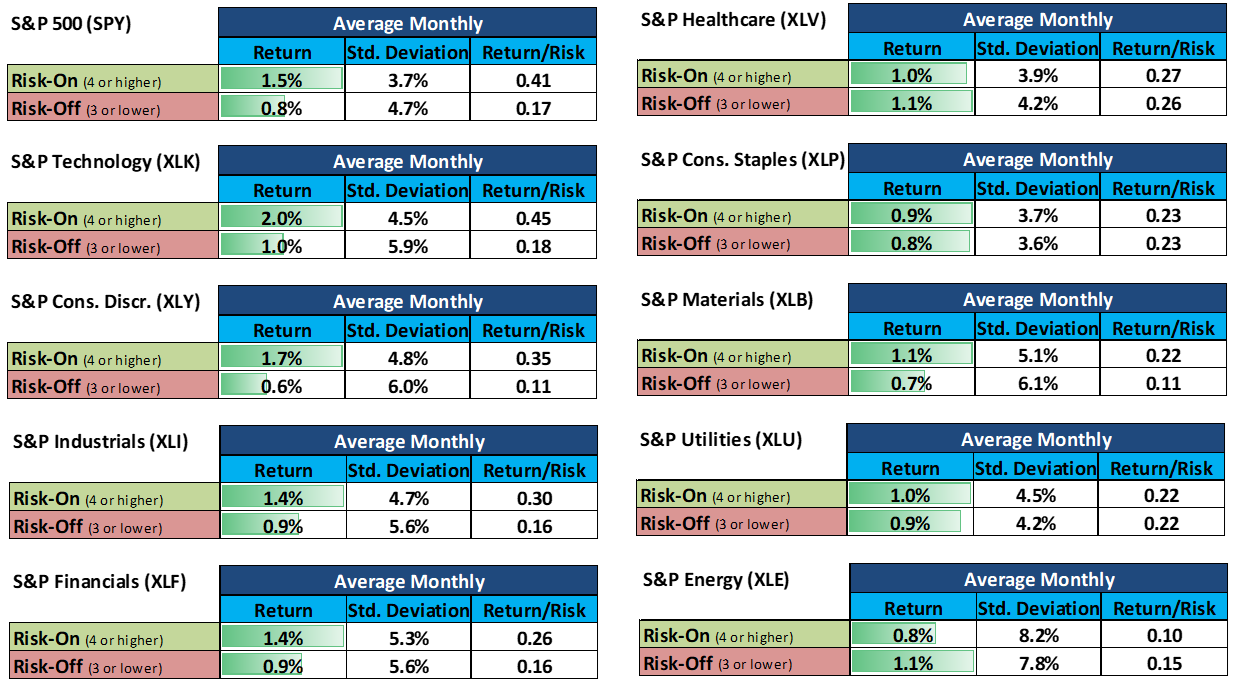

This explains why "risk-on” regimes emerge while economic headlines remain bleak. The market is a discounting mechanism that responds to the global liquidity cycle long before the general public sees "good news.” This indicator is especially valuable for managing risk-on/risk-off shifts; liquidity increasingly flows into equities, credit spreads, and speculative assets to protect the system's solvency.

Those who wait for traditional economic data to improve are usually the ones buying at the top, having missed the liquidity-driven move.

Conclusion: Navigating the Next Regime

Integrating the Sovereign Liquidity Engine into your asset allocation strategy is no longer optional. We are operating in a regime where fiscal interest costs are the primary pressure point for future policy action. As these costs rise, the expansion of the liquidity cycle becomes a mathematical inevitability rather than a policy choice.

Liquidity remains the most important driver of asset markets. It is the tide that lifts or grounds all boats, as we wrote in our previous article The Global Liquidity Cycle Explained. By looking past the headlines and focusing on the mechanical reality of debt servicing, investors can move beyond the noise and position themselves for the next macro regime.

As the Sovereign Liquidity Engine begins to rev, the critical question for every investor is this:

Are you fighting the tide of the debt clock, or are you positioned for the inevitable flood of liquidity that mathematical necessity demands?

Those who ignore the liquidity cycle are destined to be blindsided; those who understand the engine are the ones who thrive.