Ahoy!

Please note this is a lagged sample report that all LOGIC Macro Regime subscribers received well before the referenced month began.

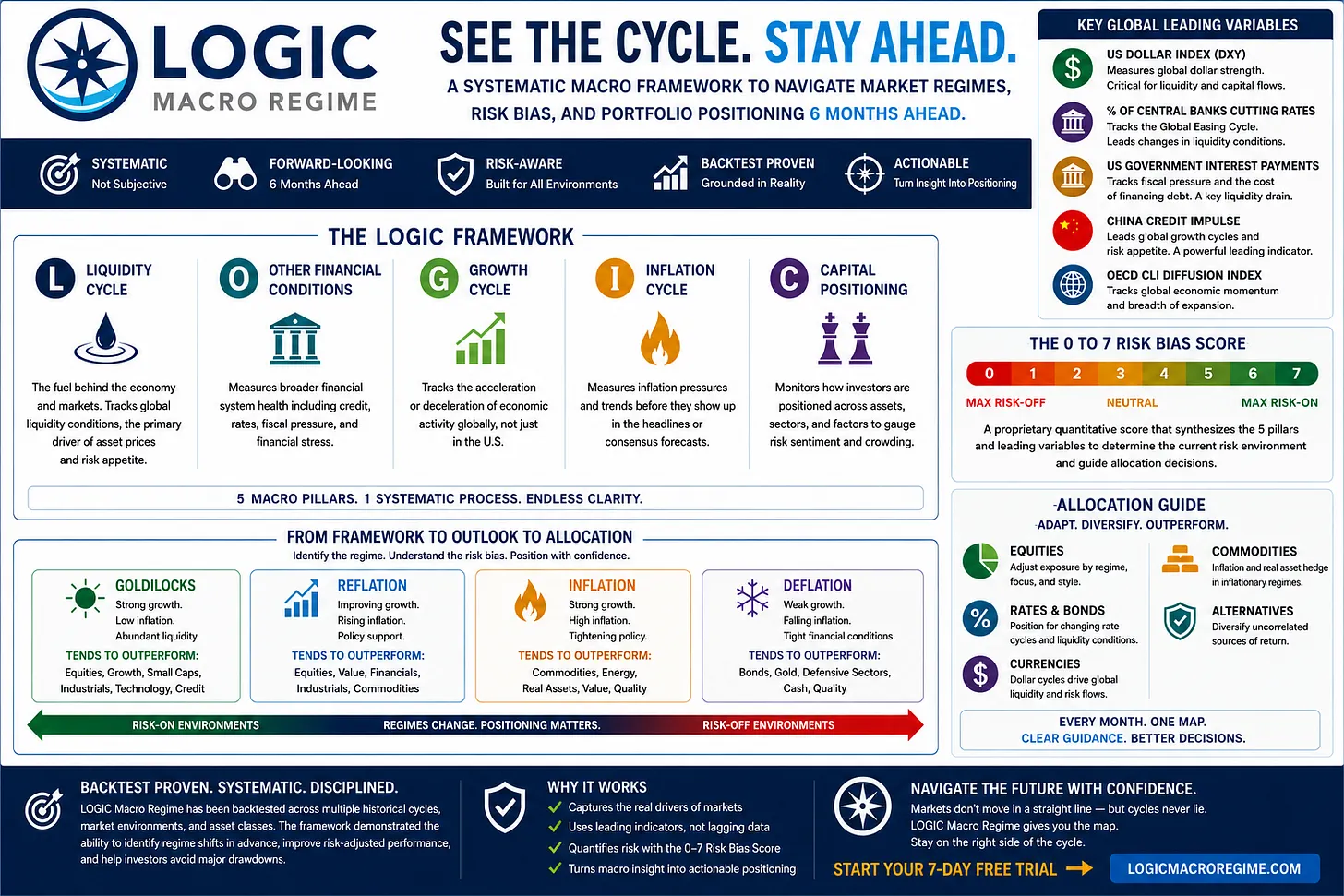

The conditions for the months ahead reflect the aggregate state of the Liquidity, Other Financial Conditions, Growth, Inflation, and Capital Positioning cycles, alongside key global leading indicators. As of today, these all point to the current LOGIC signal, which is an improvement over last month's (4) Risk-On Reflation.

June 2026 Snapshot

Forward View (6 months) April and May introduced a meaningful shift in the macro backdrop. Geopolitical tensions surrounding Iran and disruptions through the Strait of Hormuz pushed oil materially higher, lifting inflation expectations and creating a tightening impulse through financial conditions. Heading into 2026, persistent energy-driven inflation was not on the bingo card. With WTI crude holding near $100/barrel and Brent briefly surpassing $110, inflation has proven stickier than initially expected. Importantly, however, the broader message remains unchanged. We previously noted that weakness through March and April would likely represent an "air pocket" rather than the start of a broader deterioration in the cycle, and that appeared to be play out. Risk assets have remained resilient throughout the geopolitical volatility. Following a correction that pushed the S&P 500 roughly 10% below its January highs, markets recovered rapidly toward new highs, while the US ISM Manufacturing PMI climbed to 52.7 in April, its highest level in nearly four years. This distinction matters. The current environment reflects a higher nominal growth regime rather than stagflation. Growth and inflation are accelerating simultaneously, creating a Risk-On Reflation environment rather than a deteriorating macro backdrop. While less ideal than Goldilocks, Reflation remains supportive for risk assets as stronger earnings expectations and cyclical participation continue offsetting inflation pressures.

Looking ahead, the path through August remains constructive, with September to December looking to be choppier and more susceptible to a deeper Risk-Off correction. The good news is that the Macro Regime still looks favorable with Goldilocks. We'd be more concerned about a longer/more severe period of weakness on the horizon, if Inflation and Deflation coincided with Risk-Off.

(L) Liquidity Cycle ✅

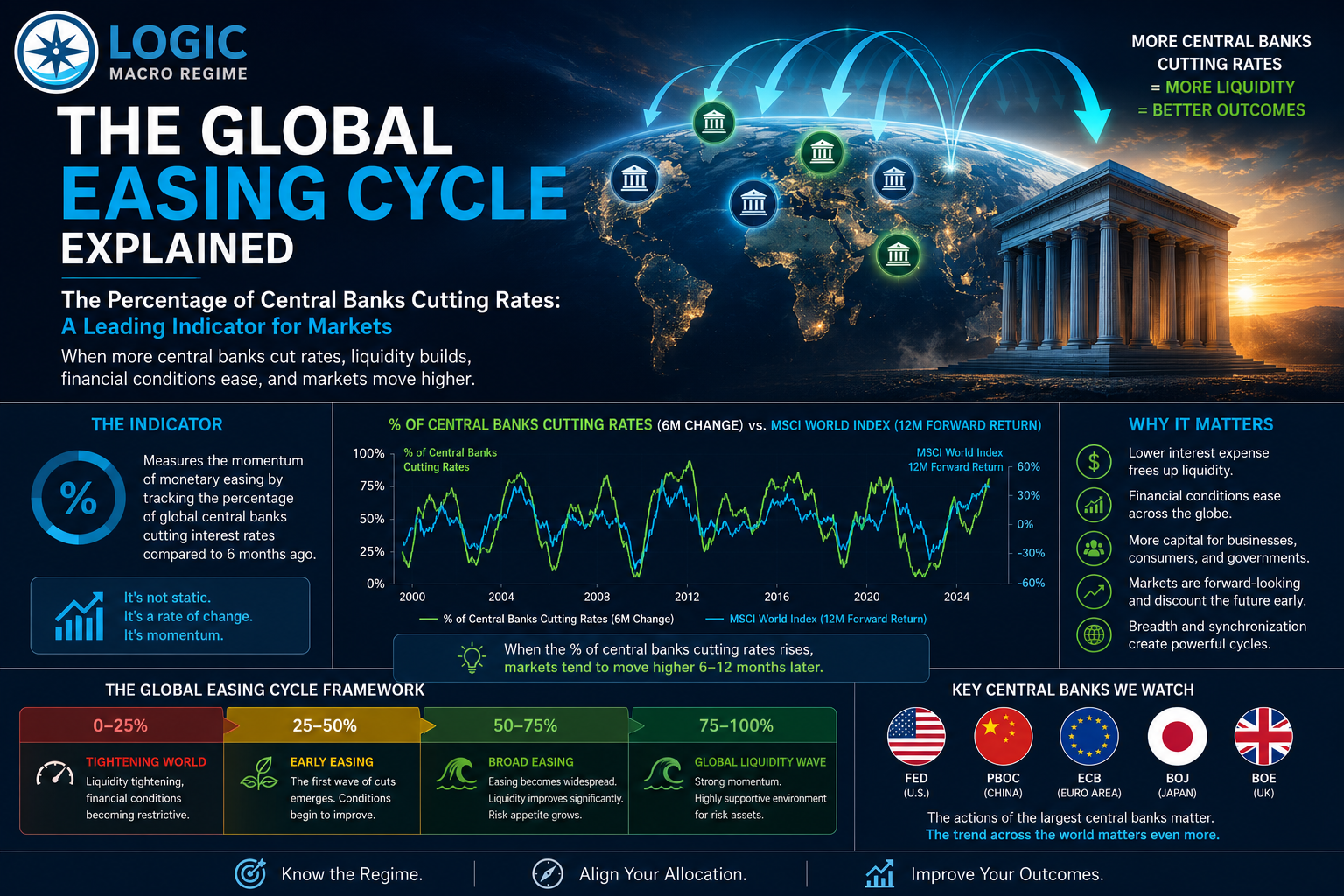

Global liquidity continues to improve and remains supportive of risk assets. Global M2 money supply growth continues running near mid-single-digit year-over-year rates, while central bank balance sheets have largely stabilized rather than contracted aggressively. Central banks remain in a maintenance phase rather than aggressively tightening policy, allowing reserves and funding conditions to remain supportive. Liquidity is not necessarily creating a new catalyst at this stage of the cycle, but importantly it also does not appear to be acting as a constraint. Real liquidity conditions remain positive enough to support continued credit creation, earnings growth and risk appetite. This remains an important tailwind supporting broader financial markets.

(O) Other Financial Conditions ❌

Other financial conditions remain the primary area of weakness. Higher oil prices, elevated bond yields and geopolitical uncertainty surrounding Iran created a meaningful tightening impulse over recent months. The US 10-year Treasury yield briefly pushed higher towards 4.7%, while higher energy prices fed directly into inflation expectations and broader macro uncertainty. Rising rates reflected markets beginning to price a more persistent inflation environment, while energy shocks filtered through input costs and inflation expectations. The good news is that some of these pressures may already be beginning to ease. Oil prices have started stabilizing, the US dollar has softened modestly and bond markets have begun showing signs of consolidation. While conditions remain tighter than they were earlier this year, the pace of tightening appears to be slowing.

(G) Growth Cycle ⬆️

Growth continues re-accelerating. The softness observed through March and April increasingly appears temporary rather than structural. Manufacturing PMIs across developed economies have broadly moved back toward expansionary territory while OECD leading indicators continue improving on a diffusion basis. Global manufacturing output recently accelerated at its fastest pace since 2021, reinforcing the view that the slowdown earlier this year represented a temporary air pocket rather than broader cyclical deterioration. This confirms the broader message that the business cycle itself remains intact and recent market volatility represented a pause rather than meaningful economic weakness. Accelerating growth alongside improving liquidity remains supportive of the current reflation narrative.

(I) Inflation Cycle ⬇️

Inflation has become more persistent than initially expected. Higher oil prices driven by Middle East tensions and supply disruptions have reversed portions of the prior disinflation trend. Energy continues filtering through transportation costs, production costs and inflation expectations. However, it remains important to focus on the rate of change of inflation rather than inflation itself. Inflation persistence today appears more commodity-driven than wage-driven, increasing the probability that inflation could moderate if geopolitical tensions ease. If a sustained ceasefire emerges, energy prices could begin rolling over, allowing inflation pressures to gradually normalize. Additionally, structural forces including AI-driven productivity improvements and softer shelter trends continue supporting the possibility that Goldilocks remains the medium-term destination. For now, inflation remains elevated enough to support a Reflation regime, but not yet elevated enough to materially threaten broader growth conditions.

(C) Capital Positioning ✅

Capital positioning remains supportive. Recent volatility triggered a healthy reset in market positioning and investor sentiment. The correction earlier this year was relatively shallow and buying activity returned quickly as investors stepped back into risk assets. The speed of the recovery suggests institutional capital remains under-allocated rather than euphoric. Pullbacks continue being met with strong buying activity rather than sustained de-risking behavior. Positioning appears significantly healthier today following the March/April reset. As we continue moving through the summer months, positioning remains constructive, though caution likely becomes more appropriate heading into the potential September to December window of weakness, that has been on our radar for months now.

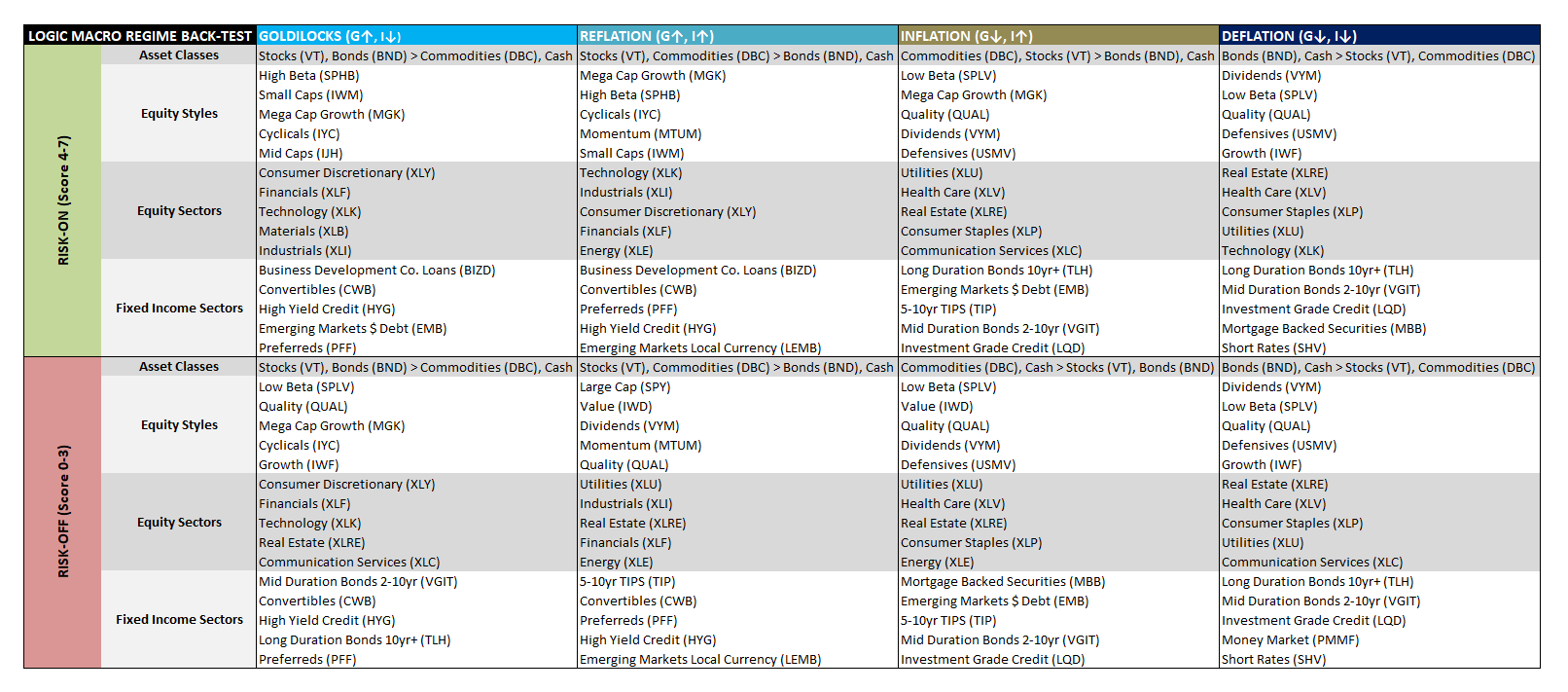

Positioning Implications

The table below can be used as a practical guide to position your portfolio across asset classes, styles, and sectors, with corresponding ETF tickers that allow you to efficiently implement these equity and fixed income tilts in real time.

With Risk-On Reflation/Goldilocks on the horizon until August, allocating to overlapping styles/sectors (in the red box) like High Beta, Mega Cap Growth, Cyclicals, Small Caps, Consumer Discretionary, Technology, Financials and Industrials, could be a favorable stock strategy along with Business Development Co. Loans, Convertibles, Preferreds and High Yield Credit, from a bond perspective. BUT, remember, don't overstay your welcome as August may be the time to start trimming back on risk, in anticipation of the September to December window of weakness. Then it will be time to review what works in a Risk-Off Goldilocks environment. Stay tuned.

For even more insight on how to position (and to see the table in a larger format), you can click on Back-Test for asset, style, and sector factors that historically have out/under-performed in this kind of Macro Regime.